Mobile Home Park Loan Checklist: What You Need to Get Your Deal in Front of Lenders

You’re under contract on a park, or you’re shopping seriously. You called a broker. They asked for “the package.” You hung up wondering what’s in the package.

Most checklists you’ll find online list every document the lender might eventually want by closing. That list runs to fifty items and takes weeks to assemble. You don’t need all that to get started.

You need seven things to get your deal in front of my lending partners.

Want the PDF version? Get in touch and I’ll send it over.

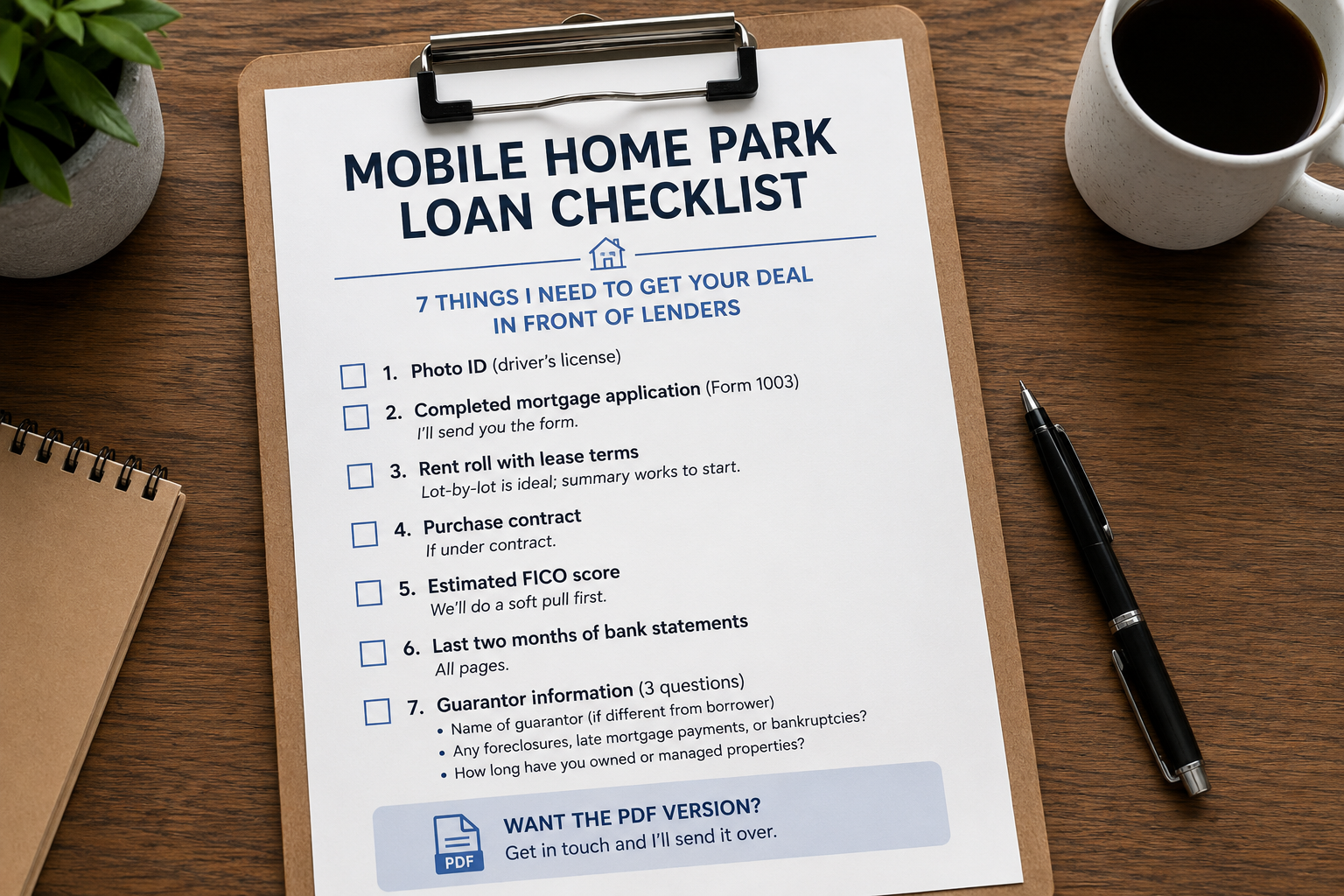

What I need to shop your deal

-

☐ 1. Photo ID (driver’s license)

-

☐ 2. Completed mortgage application (Form 1003) — I’ll send you the form. The 1003 is the Uniform Residential Loan Application, and on most commercial park deals we use it to capture the guarantor’s personal financial picture, because guarantor underwriting matters as much as the property in this space.

-

☐ 3. Rent roll — Include lease terms (month-to-month, 6-month, 12-month, etc.). Lot-by-lot is ideal; a clean summary works to start.

-

☐ 4. Purchase contract — If you’re under contract. If you’re still shopping, we can pre-qualify you on the rent roll and your numbers, then move when you’re ready to write offers.

-

☐ 5. Estimated FICO score — Just an estimate. We’ll do a soft pull first to verify, then a hard pull only when the loan is moving forward. No surprise inquiries.

-

☐ 6. Last two months of bank statements (all pages) — Confirms liquidity and source of the down payment.

-

☐ 7. Guarantor information — three questions:

- Name of guarantor (if different from borrower)

- Any foreclosures, late mortgage payments, or bankruptcies?

- How long have you owned or managed properties?

That’s it for the initial shop. With these in hand, I’ll present your scenario to lending partners and come back to you with realistic terms, likely rate ranges, and what the down-payment math looks like.

What to expect on the terms

A few things to set expectations before we start:

Loan-to-value through my lending partners runs up to about 70%. Plan on roughly 30% down to start the conversation realistically. Higher leverage is sometimes available through agency programs (Fannie Mae / Freddie Mac MHC, which can go to 75–80% on stabilized parks $1M+), but agency has its own qualifiers I’ll explain below.

Closing costs are not financeable. Plan to bring cash for third-party reports, title work, and closing items separate from the down payment.

Seller carrybacks can fill part of the gap. In some cases we can structure a seller-carried note that covers a portion of the down payment, reducing the cash you bring to close. Worth raising with the listing agent before you finalize the offer.

SBA loans are not available for mobile home parks. SOP 50 10 8 explicitly lists mobile home parks alongside apartment buildings as ineligible. (RV parks and campgrounds are different — those can qualify for SBA financing. Don’t confuse the two.) If anyone has told you SBA works on an MHP acquisition, get a second opinion before you commit.

What the lender will want next

Once a partner is interested and you’re moving toward term sheet, the lender will ask for more documents. Plan to have these ready when we get there — not now, but soon after:

Property package: trailing 12-month operating statement (T-12), two to three years of historical financials, 12 months of utility bills, property tax bills, current insurance binder, park-owned home schedule, occupancy history, photos.

Sponsor package: personal financial statement, two to three years of personal tax returns, schedule of real estate owned, brief experience summary.

Third-party reports (lender orders these, you pay): appraisal, Phase I environmental, property condition assessment, ALTA survey, title commitment. Budget roughly $15,000 to $25,000 and 30 to 45 days to complete once ordered.

You don’t need any of this at intake. We collect it as we move from term sheet toward closing.

A note on agency loans and first-time buyers

If we end up routing your deal toward agency debt (Fannie Mae or Freddie Mac MHC), there’s one qualifier worth flagging early: Freddie Mac generally expects the borrower to have at least two years of MHC operating experience and currently own at least one other MHC. Fannie Mae similarly expects at least one Key Principal with MHC experience.

For first-time buyers, that doesn’t kill the deal — but it usually means bringing in a minority partner with prior MHC experience, or routing the deal through a bridge or local-bank execution first while you build the track record. Plan for that conversation if this is your first park.

Realistic timeline

- Days 1–3: You send me the seven items above.

- Days 3–10: I shop the scenario and get preliminary terms back from lending partners.

- Days 10–21: Pick the best fit, formal application, lender starts underwriting.

- Days 21–60: Property underwriting, third-party reports completed.

- Days 60–90: Final approval, loan documents, closing.

Bridge and local-bank deals can close on the faster end — sometimes 30 to 45 days, occasionally faster. Agency deals (Fannie Mae / Freddie Mac MHC) typically run 75 to 90 days from term sheet to close but offer better long-term financing for stabilized parks at $1M+.

What to do next

Under contract. Send me the seven items above and the property address. I’ll come back within a business day with the lending paths that fit your deal and what likely terms look like.

Shopping but not under contract. Send me items 1, 2, 5, 6, and 7 — that pre-qualifies you on the sponsor side. Then we’ll know exactly what to write into your offers.

Want the PDF version of this checklist. Drop your email and I’ll send it over.

Amy Brown · NMLS #2310281 · NEXA Lending. Commercial financing available nationwide; residential licensure in MD and FL. Educational guidance only; not a commitment to lend. Terms, rates, and program availability subject to change.

Ready to discuss your park acquisition?

Get personalized financing options for your mobile home park deal.

Start Your Inquiry